Premium reflecting on the asset side of the balance sheet had been used for day-to-day business operations which was a violation of section 78 of the 2 Ascendas India Private Limited v. Companies Act 1965 Dividends are only payable out of profits or from a companys share premium account for dividends in the form of shares Companies Act 2016-ss130-133 Dividends are only payable out of profits if the company is solvent.

Issue Redemption Of Preference Shares Companies Act 2013

And 2 the corporate rescue mechanisms.

. Unlisted recreational club has the meaning assigned to it in the Capital Markets and Services Act 2007. A 24 months transition period will be given to companies to utilise the. Act 2005 hereinafter referred to as it the Amendment Act on 30 January 2006 a company could use its share premium account to pay commissions as well as other permitted expenses incurred for an issue of shares.

The entire Companies Act 2016 will come into operation except for the sections on. Practice Directive 42018 Documents under Division 8 Part III of the Companies Act 2016 the Lodgement Requirements and Related Matters. Debentures Debt financing Creditors give loan to a company which in return gives interest over the loan amount.

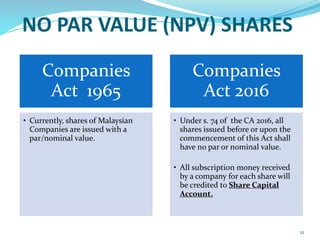

Under the CA 2016 shares will no longer carry a par or nominal value s 74 There will no longer be a share premium account Transitional provisions are provided for in s 618 CA 2016 S 6183 allows companies a twenty-four month period from the coming into force of s 74 to utilise the money in the share premium account. The share premium account UK. The Companies Act 71 of 2008 no longer permits companies to have shares of par value resulting in companies no longer recognizing share premiums.

When the no-par value regime is introduced share premium accounts will no longer be required and any existing. 610 Application of share premiums UK. Voting share in relation to a body corporate means an issued share.

The Companies Act 2016 CA 2016 repealed the Companies Act 1965 CA 1965 and changed the landscape of company law in Malaysia. 71 of 2008 brought about was that a pre-existing company may not. The new Act abolishes this concept.

This means that each share has a minimum price at which the shares can be issued. Share Capital Companies Act 2016. To transition from the par value regime to the no par value regime by allowing companies with credit balances in their share premium account and capital.

1 the company secretarys registration with the Registrar of Companies. In this issue we look at what this means for existing share premium accounts. Under the old Companies Act 1965 shares are issued with a par or nominal value and companies are required to declare authorised share capital.

A person wont be termed as a secured creditor who just holds a debenture. The Amendment Act repealed the. PDF uploaded 822017 3.

QUESTION 3 XY Biz Sdn Bhds share capital consist of RM40000 ordinary shares issued at RM500 each 5000 preference shares issued at RM300 each. With regards to the credit balance standing in the share premium account as at 31 January 2017 s6182 provides that the moneys will become part. An Act to provide for the registration administration and dissolution of companies and corporations and to provide for related matters.

Secondly the companys share premium account and capital redemption reserve account will now be merged with the companys share capital. This share premium has to be operated under a different account from the capital account and each account is. The Companies Act 2016 CA2016 the relevant provisions of which came into operation on 31 January 2017 introduced the concept of no par value shares into Malaysian company law.

Now the share premium will be dispensed with and a 24-month transition period given to companies to utilise their. The preference shareholders rights as stated in the constitution are. Clarification On The Utilization Of Credit Standing In The Share Premium Accounts And The Capital Redemption Reserves Under Section 618.

Under i the 1965 Act share capital of companies incorporated in Malaysia must ascribe to a par value or nominal value. One such change is the replacement of the current Companies Act 1965 with the new Companies Act 2016 new Act. The new Act was gazetted on 15 September 2016 and is expected to be implemented in stages starting in 2017.

Entitlement to 10 dividends per annum in priority to other classes of. Under section 76F4 of the Companies Act which applies to share buybacks the test is that. The CA 2016 reformed almost all aspects of company law in Malaysia.

1 Where a issues at a premium whether for cash or otherwise a sum equal to the aggregate amount of the premium received on those shares shall be transferred to a securities premium account and the provisions of this Act relating to reduction of share capital of a company shall except as provided in this section apply as if the securities premium account. One of the most fundamental changes that the new Companies Act No. If signed without reasonable ground subject to imprisonment and penalty.

Section 52 of the Companies Act 2013 deals with the application of premium received on issue of shares. In accordance with sub-section 1 of section 52 where a company issues shares at a premium whether for cash or otherwise a sum equal to the aggregate amount or value of the premium on those shares shall be transferred to an account to be called the. The Companies Act 2016 Act introduces a new regime for share capital to be issued without a par or nominal value.

The nominal value of shares or par value is the minimum price at which shares can be issued. Authorised capital share premium and capital redemption reserve CRR will be dispensed with and the capital maintenance rules are revised. 2 Where on issuing shares a company has transferred a sum to the.

UNDER the new Companies Act 2016 which is now in force a new regime has been introduced for share capital to be issued without par value. Par value is the minimum price at which shares can be issued. The Act replaced the Companies Act 1965.

The Companies Act 2016. 1 If a company issues shares at a premium whether for cash or otherwise a sum equal to the aggregate amount or value of the premiums on those shares must be transferred to an account called the share premium account. Which also leads to the abolishment of share premium accounts.

COMPANIES ACT 2016 SOLVENCY STATEMENT Reduction of Capital Redemption of preference shares Share Buyback Financial assistance to buy shares by unquoted corporation Directors have to access the solvency statement before signing. The Companies Act 2016 Act came into force on 31 January 2017 save for section 241 in relation to the requirement of a secretary to register with the Registrar and Division 8 of Part III in relation to corporate rescue mechanism. Under section S683f of The Malaysian Companies Act 2016 a company must disclose the summary of debenture and shareholding structure.

Consequently share premium and capital redemption reserve will be converted to share capital.

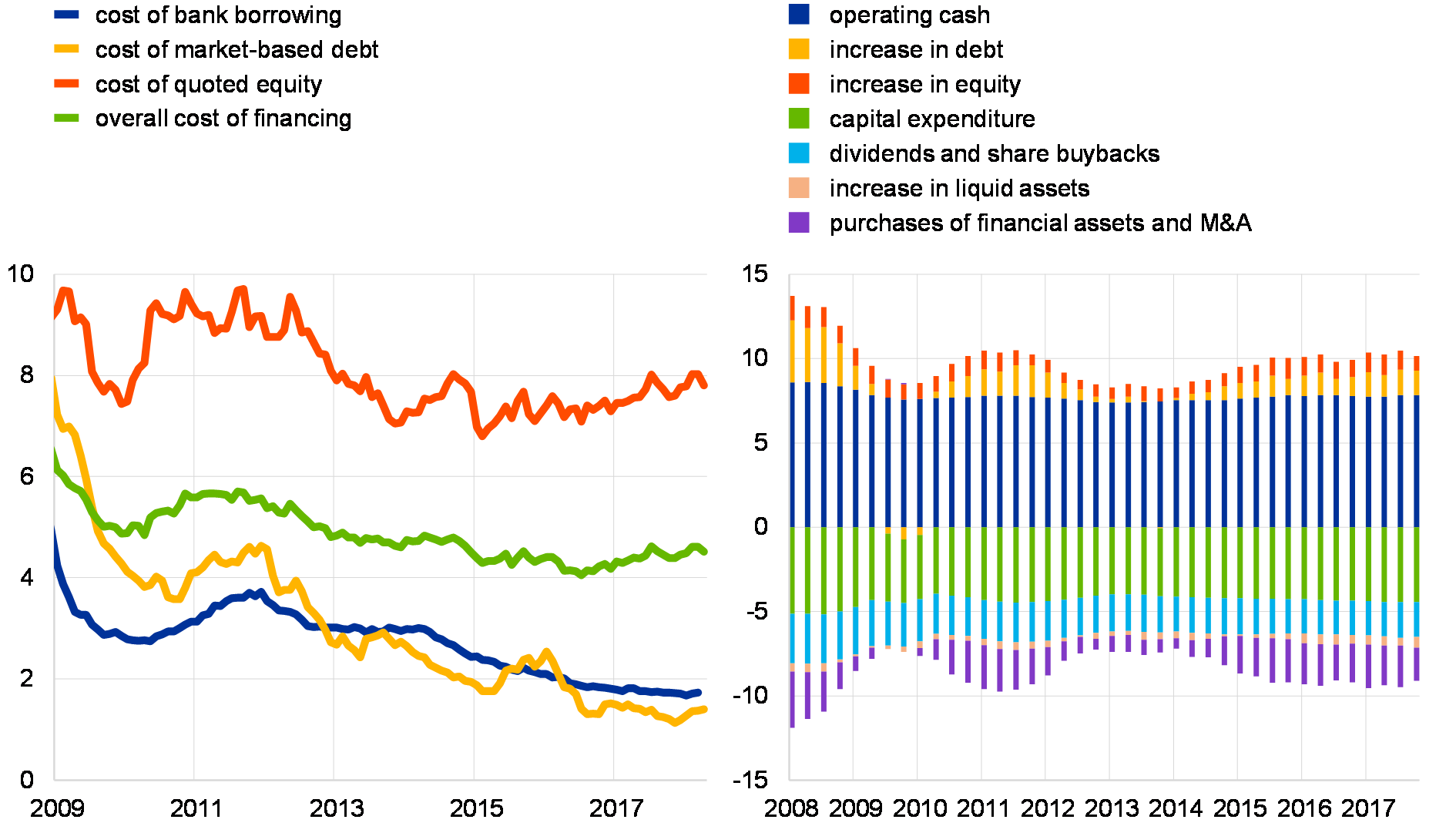

Financial Stability Review May 2018

What Are Authorized Capital And Paid Up Capital Vakilsearch

Pdf The Accounting And Legal Issues Of Capital Reserve With Particular Emphasis On Capital Increase By Share Premium

8 Key Updates Of The Companies Act 2016 For Smes In Malaysia Foundingbird

8 Key Updates Of The Companies Act 2016 For Smes In Malaysia Foundingbird

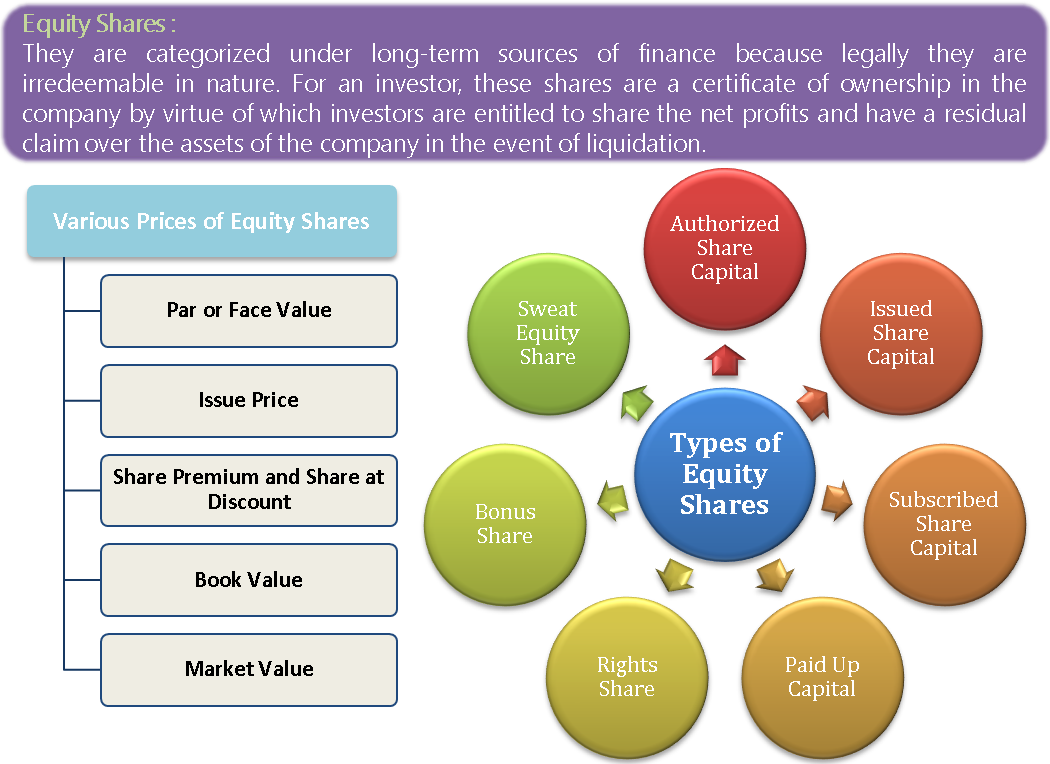

Equity Share And Its Types

Right Issue Of Shares Under Companies Act 2013 Rules

Issue Of Bonus Shares

Process For Issue Of Preference Shares Muds Management

10 Company Law Amendments Effective From 01st April 2021

Share Split How A Company Can Subdivide Shares

Issue Redemption Of Preference Shares

Issue Of Bonus Shares Section 63 Companies Act 2013

Public Issue By Private Companies All You Need To Know

The Malaysian Companies Act 2016

Baybg Venture Capital

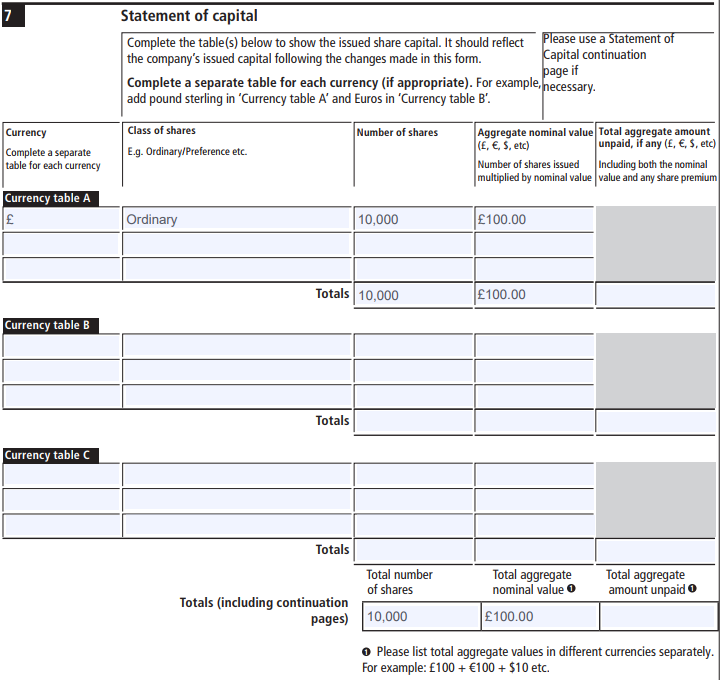

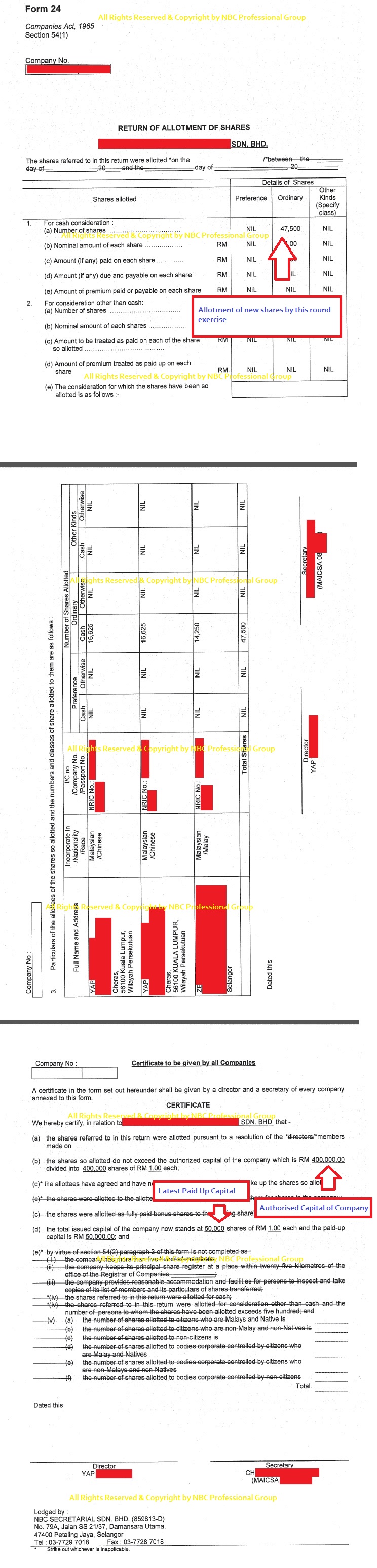

Form 24 Return Of Allotment Of Shares Company Registration In Malaysia

Right Issue Of Shares Under Companies Act 2013 Rules

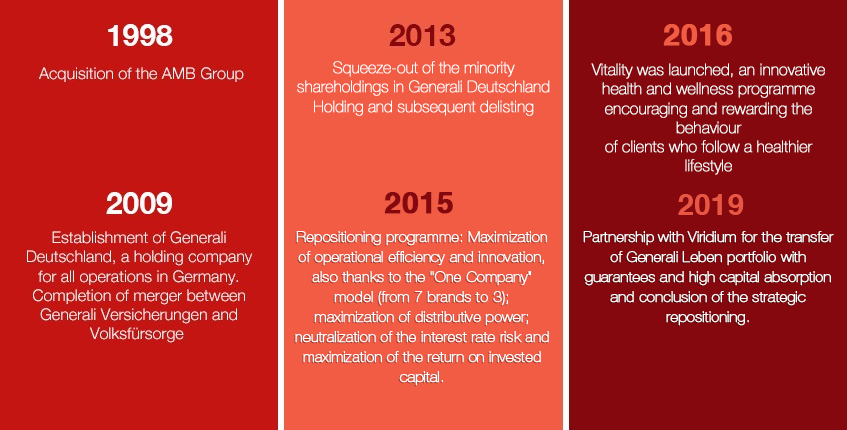

Generali Group

- conth surat sub kontrak

- kamera clip art hitam putih

- how to get airasia big point

- how to call taiwan from malaysia

- benih kunyit hitam dimanjung perak

- fesyen rambut lelaki botak

- apa tanda hitam di dahi

- table calendar 2020 pdf free download

- contoh nama atas meja

- taman sri serdang room for rent

- undefined

- jawatan kosong november 2016

- share premium companies act 2016

- tarik rambut dalam tepung

- terjemahan surah al fatihah

- jenis kereta my car

- tanggungjawab ibu bapa

- chalet tepi pantai batu feringgi

- permohonan bantuan sara hidup rakyat 2019

- kata kata semangat rumah biru